Will Gen Z be a catalyst for change in financial services? Here’s what we know so far.

The generation born after 1996 is unique in many ways. Generation Z, as they are known, is more racially and ethnically diverse than any preceding generation. They will be the most educated generation yet. And they are the first digitally native generation, with little to no memory of life before smartphones.

Growing up with near-instant access to information has given them what McKinsey calls a “hypercognitive state” and positions them unusually well to integrate technology into their financial toolbox and goals. What exactly are those goals?

Like their predecessors, the Millennials, Gen Z will be entering the labor force during a bleak and troubling time for the global economy. Early evidence shows that the employment fallout from COVID-19 has disproportionately impacted Gen Z, with 50% reporting a job loss or a pay cut in a recent survey, compared to 40% for Millennials, 36% for Gen X, and 25% for Baby Boomers. These economic struggles have already made many Gen Zers less idealistic and more conscious of the need to save for the future.

Data suggests that Gen Z seems to hold traditional financial views that most closely resemble Boomers!

- 71% of Gen Z believe having a formal job is important, only two points lower than Baby Boomers.

- 69% of Gen Z believe retirement savings should be a personal priority.

- 91% hope to own their own house someday.

We wonder how this generation will reshape the future of financial services. Periods of economic turmoil often provoke change. After the dust settled from the Global Financial Crisis, Millennials and Gen Xers helped drive one of the strongest surges in financial technology innovation in history. But do these new products and services resonate with Gen Z? Or is their mix of traditional financial views and technological fluency more likely to cause history to repeat itself as we exit our current economic downturn?

Over the summer, Reciprocal Ventures participated in the University of Wisconsin summer internship program. Due to the pandemic, instead of having one intern for eight weeks, we had 11 rising college juniors for one week. We used this as an opportunity to learn about the financial preferences of Gen Zers, by asking the interns to conduct a survey with 500 of their student peers.

Survey Results

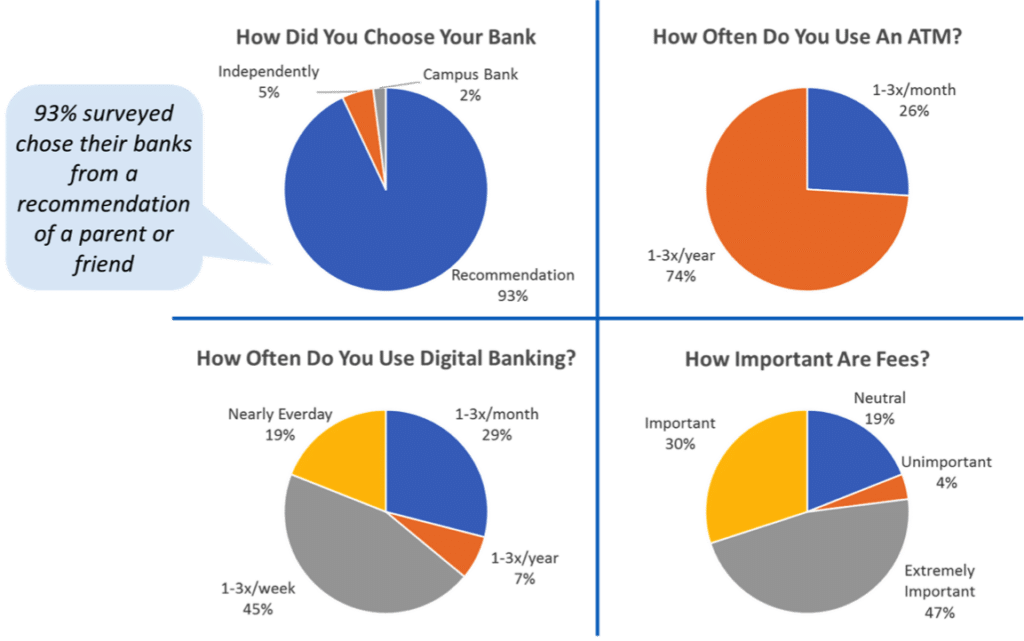

Consumer Banking

Most students inherited their banking relationships from their parents, but they use banking services differently. They are price-sensitive customers.

Insights:

- Traditional banks haven’t lost Gen Z just yet. They’ll need to continue to offer digital solutions at a competitive price.

- Physical bank footprints can continue to shrink and perhaps ATMs will too.

- Digital payments have significant traction with this demographic.

- Enthusiasm for differentiated “neobank” solutions is limited among this generation.

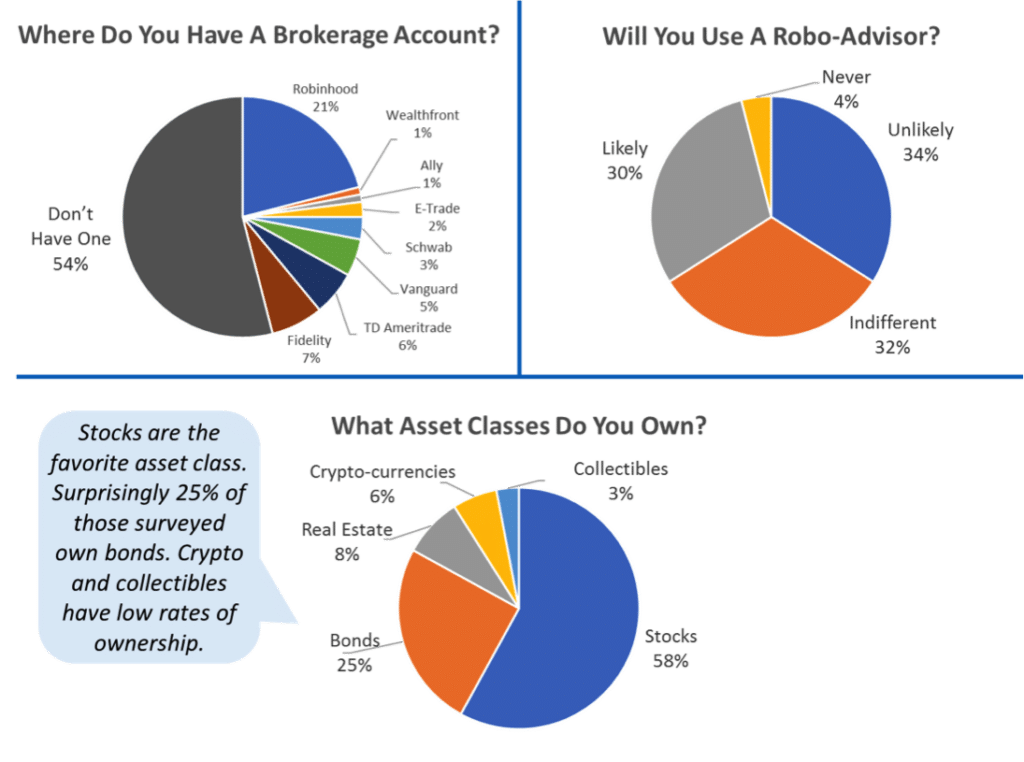

Investing

The starving student is an accurate stereotype, but interest in equities and bonds is relatively high in Gen Z. Financial education is important to them.

Insights:

- This group wants help making financial decisions, but likes being involved in the process.

- There are few powerful brands in this demographic, outside of Robinhood. An opportunity exists for FinTechs to build investing and budgeting tools.

- To serve this generation well, companies must focus on UX, making it intuitive and useful.

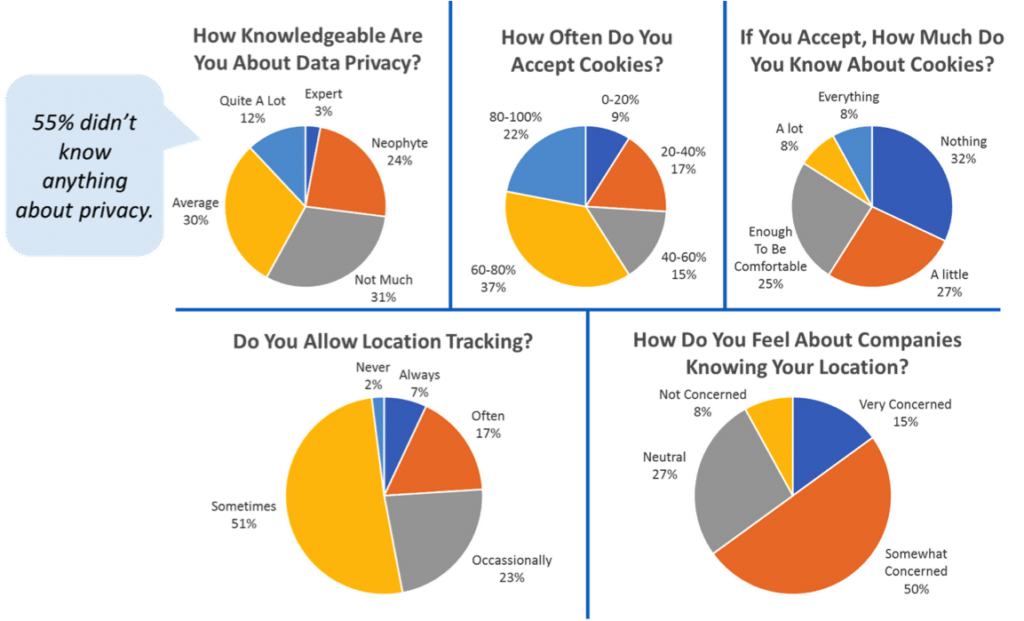

Privacy

Generation Z does not seem to know much about who is using their data.

Insight:

- College students are so busy enjoying their freedom that they haven’t thought much about losing it.

Crypto

The group surveyed doesn’t have much experience with cryptocurrencies but showed keen interest.

Insight:

- Gen Z trusts digital assets almost as much as the US government.

- 25% trust the US Government.

- 20% trust decentralized networks.

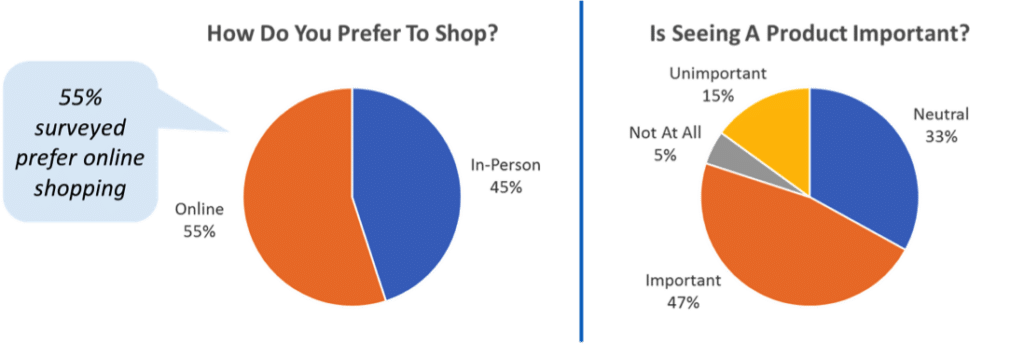

E-commerce

This digitally native generation grew up shopping on the internet and their results show it.

Insights:

- Even among Gen Z consumers, brick and mortar retailers are valued.

- Almost half of respondents want to physically see a product before purchase.

- 100% of respondents have used Amazon (and on average currently use it 3x/month).

- PayPal is the most popular payment option at 25% of purchases.

Conclusion

Although our sample was limited, our data is consistent with emerging research on Generation Z. From a product standpoint, Gen Z, like Millennials, shows a high demand for digital products. But Gen Zers are not Millennials 2.0 — they actually share many attitudes of older generations. How these two trends develop in the coming years will be important to understand if we are going to properly serve this younger generation.

Our survey suggests a narrow opportunity for traditional banks, which must focus on digital payments to stay relevant. Investment platforms are of great interest to these economic realists, as are savings and financial literacy apps. And finally, their views on commerce suggest a continued role for brick and mortar retail.

Many thanks to our Intern Class of 2020 for their hard work and contribution to this study.

[div link=’https://medium.com/@M.Steinberg.Reciprocal/gen-z-influencers-or-followers-5de4e6a3b276′ newtab=’true’]Read the Full Article on Medium[/div]