The recent launch of FedNow in Q3 of 2023 has sparked optimism that there will be a surge in real time payments in the U.S. FedNow has been long awaited, but it is unknown if this new program is overhyped or if we truly are on the verge of a payments transformation. This new, advanced, and faster payments system also raises the question if crypto has a place in the future of payments? We’ve been investing in the payments sector at Reciprocal Ventures for the past seven years and wanted to address this interesting question.

What is FedNow?

FedNow is the Federal Reserve’s new, real-time payment scheme that allows instant, irrevocable, 24/7/365 payments between domestic bank accounts. FedNow is a new payment rail that banks and credit unions can use to enable faster payments for customers.

FedNow is both faster than ACH payments and cheaper than wire transfers. Those legacy solutions typically process payments in batches and have specific operating hours, resulting in delays and restricted access to funds outside of regular banking hours. FedNow will handle only domestic credit transactions (“push payments”), not debit (“pull payment”) authorizations. Push payments allow for payment finality just like with wires, and there is no risk of payments failing due to insufficient funds.

A feature of FedNow is a Request For Payment or RFP, which is an improvement on ACH debits. RFP is a simple way for a person or organization to present a bill to a customer through their mobile banking app and request an instant payment. The customer can then approve the pre-filled information about the payment amount and push a payment to the biller in a single step. We anticipate a new set of value-added payment services built on RFP will be a meaningful accelerant for FedNow use.

Existing Payments landscape

In the traditional payments landscape, FedNow will join RTP (Real Time Payments) and Visa/MasterCard Original Credit Transaction “OCT” in enabling faster payments. The RTP network, run privately by The Clearing House, is available to banks, but adoption has been limited and lopsided since there are only a few senders of RTP payments. While 300+ banks can receive RTP payments, only ~30 of the largest banks can send RTP payments. And of those roughly two thirds of the RTP sending banks are shareholders in The Clearing House. Growth for RTP has been steady, but after five years, RTP payments are still only a small piece of the overall payments mix in the U.S., with $29 billion in payments value processed in Q2 2023.

Where FedNow fits in

FedNow is designed to be accessible to all US financial institutions. The system will leverage the existing nationwide payment infrastructure and established customer relationships of the Federal Reserve, which has more than 10,000 depository institutions in its network. This should make it easier for more banks to support FedNow than RTP, and expand the reach and use of real-time payments.

In practice, FedNow can provide customers immediate access to funds, move money more efficiently and support time sensitive transactions. We think the most promising near term use cases will be in (1) instant funding of new accounts (trading platforms, neo banks), (2) customer approved bill pay (single bills, credit card payments), (3) customers control a platform account (i.e., eBay, Stripe), but need money rapidly in their bank account, and (4) businesses disbursements (e.g., payroll, insurance payouts, loan payouts, etc.). Further out, business-to-business payments (A/R and A/P) are a ripe use case, benefiting from speed, enhanced liquidity, and finality of payment.

We anticipate FedNow will have an array of wide-reaching externalities to the payments landscape. Accelerating payments in the use cases above will have a large impact. All will speed up the velocity of money, causing bank deposits to ebb and flow more quickly. This could further destabilize poorly capitalized banks. Reducing payout times will also rob banks of 24-48 hour periods of float, where they generate income by investing customer funds in overnight repo or money market accounts. It will also help to accelerate time to revenue for startups and other businesses that are rapidly acquiring customers. Coinbase, for example, currently takes up to two weeks to receive initial funding of accounts.

Challenges to mass adoption

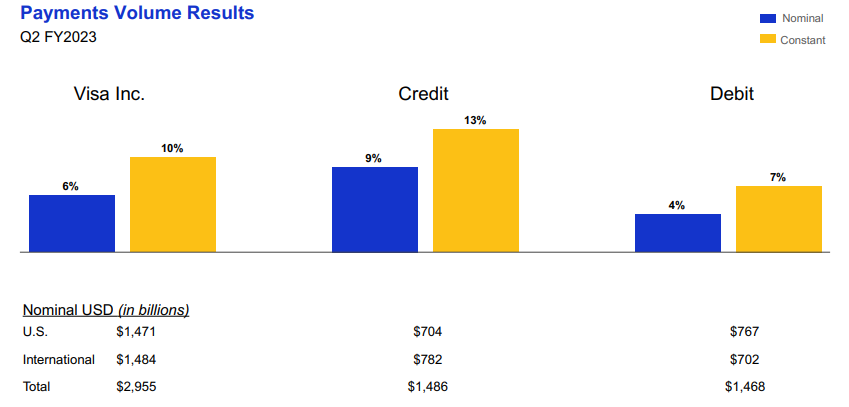

In order for FedNow to live up to its potential, broad bank participation, higher transaction limit thresholds, and rich data provided by FedNow will be crucial for business payment adoption. On the consumer side, the application to retail payments and displacement of cards is less clear. Consumers love their plastic cards, and volumes continue to expand as seen in the chart below, where Visa delivered 10% y/y payment volume growth on a constant basis in Q2. It may face a similar fate as pay-by-bank (ACH) at point-of-sale, which still suffers from poor user experience (e.g., account details, slow transaction times, limited incentives) and has not reached meaningful levels of adoption. This gap has spurred a herd of Fintechs chasing the opportunity and time will tell if the roll out of FedNow accelerates these trends, but we aren’t counting on it in the near term.

Source: Visa Fiscal Third Quarter 2023 Financial Results.

We expect FedNow will be slow to launch, as banks get on-boarded, technology and connectivity comes to market, and standards are developed. The certification process with the Fed may also take a number of banks out of the running. Additionally, the slow pace of payments adoption in banks has a large link to the banking cores – both the technical lift as well as the cost in implementing has been a big factor. For FedNow to take off, implementation will require coordination across a variety of stakeholders, and we see opportunity in the solutions that will accelerate its adoption. Faster payments also invites faster fraud, which is becoming a sensitive area for the ecosystem on the heels of launching. Focus will prioritize security and fraud safeguards as non-reversible payments proliferate, which should deliver commercial opportunities for new and existing fraud solution providers. With its launch, we’re excited about Fintechs, payment companies, infrastructure providers, and software companies that will help implement FedNow into legacy or new payment solutions for businesses & consumers.

How FedNow impacts Crypto

Advocates of cryptocurrencies have made a lot of promises about its ability to transform the traditional payments industry. However, many of those promises remain unfulfilled. Outside native web3 participants, few have made the leap to pay on crypto rails.

In the web3 ecosystem, there is a disconnect between the speed and accessibility of fiat and blockchain-based payments. It’s slow to get your money into the ecosystem at the size you want, but once in crypto, payments are fast. You could be waiting days for a bank transfer to clear access to your digital assets. This delivers a poor experience for the customers of on/off ramps, exchanges, and custodians. FedNow can accelerate on and off ramps in general which we think could considerably enhance user experience and increase the velocity of business on web3 platforms. We’ve laid out the primary feature comparisons of these instant payment technologies below.

What does this mean for stablecoins?

| FedNow | RTP | ACH | Stablecoins | |

| Speed | Real-time (instantaneous) | Real-time (instantaneous) | 1-3 business days (batch processing) | Near-instant (blockchain-based) |

| Availability | 24/7 365 days | 24/7 365 days | Bank hours | 24/7 365 days |

| Transaction cost | 4.5 cents per transaction | 4.5 cents per transaction | 0.5 cents per transaction | Close to zero, dependent on blockchain network fees |

| Access | Bank only U.S. | Bank only U.S. | Bank only U.S. | Non-restricted Global |

| Push vs. Pull | Push and request for payment | Push and request for payment | Push and pull | Push and smart contract based pull capabilities |

| Transaction limits | $500,000 | $1,000,000 | Up to $100,000,000 for batch ACH $1,000,000 for same day ACH | No specific limit |

There are two types of stablecoins: centralized and decentralized. Both are permissionless and pseudonymous, provide open access and degrees of privacy, but have different architectures and tradeoffs.

Centralized stablecoins like USDC are centrally controlled by business entities whose primary objective is profit. They are backed by reserves held by a custodian or bank. The most common collateral is USD, but other reserves include EUR, gold, diamonds, etc. Because these entities are centralized, they have the power to censor transactions and even freeze coins.

Decentralized stablecoins, like DAI which is backed by a variety of digital assets and other mechanisms, are truly decentralized and peer-to-peer. No single entity can freeze tokens the way a centralized issuer can, and privacy is preserved.

While there are tradeoffs between the two, the value proposition of a permissionless, fast, and cheap way to send digital dollars is compelling. In 2022, transaction volume on the largest stablecoin, USDT, was $18.2 trillion, exceeding $14.1 trillion in transaction volume on the Visa Network. The primary use of stablecoins today is to transact in digital goods; buying NFTs, purchasing cryptocurrencies, etc. Peer-to-peer transactions are another use, and are as easy as using Venmo or Zelle, but stablecoins offer additional privacy advantages, as the two counterparties to a transaction are only wallet addresses. These privacy advantages have experienced limited market demand.

With the launch of FedNow, the instantaneous and affordable aspect of stablecoin’s value proposition is no longer as unique.

FedNow plays in its own domestic sandbox, so if stablecoins once held domestic promise or relevance for broader uses, that window of opportunity is closing. There is stablecoin opportunity on the domestic front by serving the needs of the unbanked, as well as use cases in enhancing corporate treasury management.

On the other hand, we think stablecoins have found a wedge in global use cases. Domestic payment systems like FedNow are walled off from each other and do not have global reach. Global payments involve the coordination of numerous intermediaries, and the entire process can be expensive and slow. In this model, banks are the gatekeepers and take custody of all funds. This is where stablecoins can step in.

Where stablecoins can thrive

Stablecoins like USDC enable open access, payment finality, self-custody, and the transfer of value to anyone, anywhere. Stablecoin payments are fast, cheap, 24/7/365, and peer-to-peer, reducing the need for banks. As a bridge currency, stablecoins can connect closed payments systems and international markets. Stablecoins are increasingly being used for cross-border transactions and remittances as a fast and cost-effective means of payment. In addition to cross-border, stablecoins are finding use in the areas of dollarization and financial access. In high-inflation, unstable countries like Venezuela and Argentina, for example, people are eager to seek rescue in stable foreign currencies, where USD-pegged stablecoins are used for protecting savings from inflation as well as for daily purchases. These use cases are novel and highly valuable to distinct user groups, but given their nascency, likely represent a smaller potential opportunity in the near term than cross-border. We expect these trends to accelerate as the ecosystem builds up.

Final thoughts

Both FedNow and cryptocurrencies represent significant innovations in faster digital payments. While FedNow is a grand and ambitious project, it still has gaps and limitations which cryptocurrencies were inherently built to resolve. FedNow can provide an on-ramp to digital payments for individuals and businesses within existing financial structures. In parallel, cryptocurrencies continue to push the boundaries of innovation and offer a decentralized global alternative for those seeking more autonomy and flexibility around their financial transactions.

In the end, the world of digital payments will not be a winner-take-all system but rather a hybrid model. A system where the strengths of each FedNow and crypto are leveraged to create a more inclusive and efficient financial ecosystem.

—

Special thanks to the larger Reciprocal Ventures team, for all the thoughts, feedback, and support on this post.

And stayed tuned for “Part II: Crypto Payments Market Map.” If you’re building in the crypto payments space or would like to collaborate on the topic, please don’t hesitate to reach out to [email protected].

Tweet